Customer expectations have always been mending, but this technology tsunami is a completely new phenomenon on the contemporary financing horizon. The Banks are pushed to the wall by extensively mushrooming competitors and rigorously reforming regulations.

Amidst the rising fracas, two prime proceeds are certain: the role of these new technologies will increase and the regulations to curb their misuse will get more stringent. The change is exhaustive and will shake and stir all sections of this wide old giant sequoia right from the deepest roots to the crown.

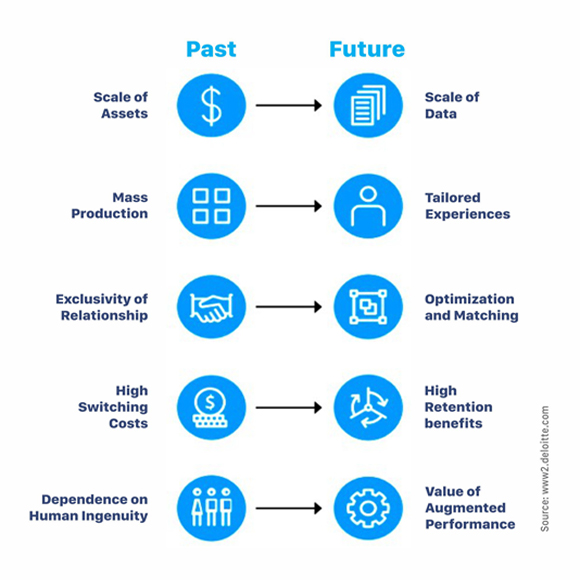

The most profound effect, however, can be seen in AI’s dismantling of the conventional tradeoffs between service quality and cost. In this new technology-powered scheme of things, manual operational efficiency will become redundant as a competitive differentiator. And as the market shifts its focus from financial institutions to service providers, the above agents (AI, machine learning and, data analytics) work toward a singular aim — Survival of these institutions.

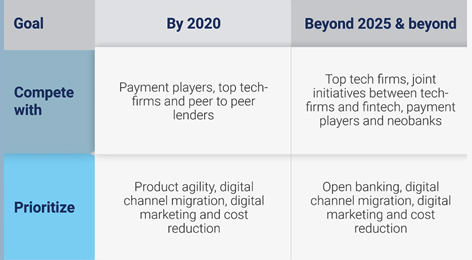

In the present metamorphosing business environment, banks are compelled to reform their business models, products and services and they have to re-think their investment priorities. Present trends point to short-term and long-term goals:

Banks are increasingly using AI and machine learning for: constructing rich data sets to help fight fraud, automating back office functions to save customers’ time and money, processing automation for trade finance, smart contracts, foreign payments and KYC process. AI is helping automate routine transactions like refinancing and bill payment. The resultant benefits are groundbreaking. Reuters, in its 2017 said, The Bank of New York Mellon Corp reported a profit of USD 300,000 by shifting its manual process to automated processes. It also reported 100% accuracy in account-closure validations across five systems, 88% improvement in processing time, 66% improvement in trade entry turnaround time, ¼-second robotic reconciliation of a failed trade vs. 5-10 minutes by a human.”

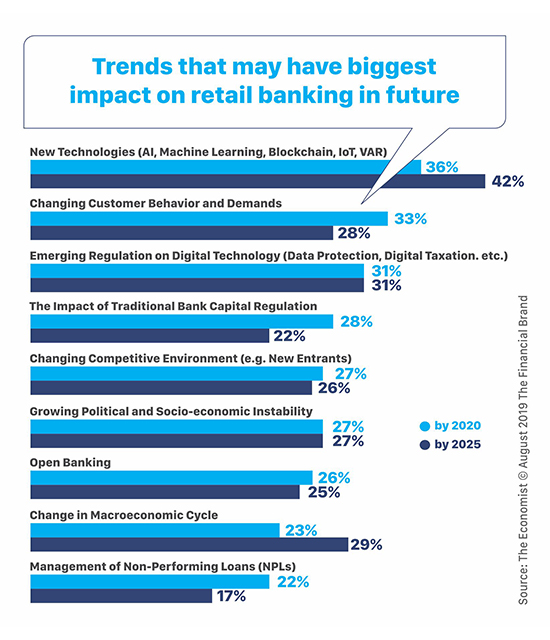

Hyper-personalization will steadily spike between 2020 and 2025 and is expected to grow from the current 19% to 24%. IDC, in its 2018 report, Worldwide Public Cloud Services Spending Forecast to Reach $160 Billion This Year, says present cloud infrastructure accounts for 1/3rd of the total IT spending on financial services. The spending is expected to continue growing at 20% + CAGR.

Two extremities of profit generation and cost-cutting spearhead technological upheaval. AI is addressing the challenge in a multi-layer fashion. It has found its roots in almost in a wide array of banking operations including but not limited to accounting, cybersecurity, merchant services, compliance, risk management, credit assessments, wealth and asset management, customer service, sales and marketing, infrastructure security and audits. In its two-pronged approaches, it optimizes performance and productivity and, lessens costs.

Conventional financial product advice has been essentially generic and impersonal. It was difficult to pull both the product and the customer information and synthesize the best solution. In AI-based self-driving finance solutions, the customers can interact with the AI-based agent and can get the most suited customized advice. At present, the bulk of these solutions is focused around homebuying, corporate financing and retirement planning.

Banks will have to innovate. These can reinforce their footing by:

The good news is they are already doing so. 41% of financial institutions are planning to extend their digital ecosystem beyond offering their own products and services. This includes third-party banking and adding non-banking products and services. Open banking and cloud show tremendous potential. The data sharing and security aspect of Open Banking, however, needs to be pondered upon. The accountability weak link in algorithm-based decision making has to be resolved.

Banks can either choose to become a multi-service provider collaborating with various agencies or they can carve a niche segment for themselves. AI can improve the footing of the existing big players and provide a fertile ground for niche players. Mid-size firms, however, may see a difficult time ahead.

Don't miss this opportunity to share your voice and make an impact in the Ai community. Feature your blog on ARTiBA!

Contribute

The future is promising with conversational Ai leading the way. This guide provides a roadmap to seamlessly integrate conversational Ai, enabling virtual assistants to enhance user engagement in augmented or virtual reality environments.